|

Tuesday 31st August 2021

Hi Friend,

TSE Deep Dive ...

|

|

|

The Saturday Economist Club ... Financial Markets and Our Deep Dive ... |

|

|

The Saturday Economist Club Deep Dive ...

My thanks again for Subscribing to The Saturday Economist Club. I hope you enjoyed the Bank Holiday Weekend, avoiding the traffic if possible.

It was great to take a short break from economics for a few weeks. I say break, the data sets are always maintained. It was also a chance to work on our new series on Digital Accommodation. I thought I would include some of the charts in our Deep Dive this week with some comments for your information.. As always if you have any queries, just let me know. Or anything you would like to see covered, likewise ...

|

|

|

Inflation CPI Basis ..2.0% in July ...

Just as markets are fretting about prices, inflation CPI basis slowed to 2.0% in July. The surprise drop in service sector inflation the culprit. Goods inflation remained above target at 2.5%.

We expect levels to peak in August and September at just over 3% before easing slightly to the end of the year. Most analysts expect inflation to average 3% in the final quarter. The more bearish suggest price levels could be higher at around 3.7%. It promises to be an interesting call ....

|

|

|

Producer Prices up 4.9% ... Input costs up 9.9% ...

Producer price data was revised in July. Output prices increased to 4.9% from 4.5% prior month. Input costs hit 9.9% easing slightly from the May peak of just over 10%.

Oil and commodity prices largely the determinant of price levels. Oil closed over $72 dollars per barrel Brent Crude basis. Our benign outlook for inflation is undermined if oil holds above the $70 dollar level.

|

|

|

Earnings hit 8.8% in July ...

Average weekly earnings increased by 8.8% in July. Private sector earnings increased by 10.2%. This seemed a little alarming and rather unusual. Talk of £50,000 lorry drivers and bonuses for hospitality workers may provide some justification.

We decided to dig deeper and look at the comparison over the past year. Currrent levels compare with the depths of lock down last year. The trend rate of growth has been restored. We expect earnings to ease towards 3% in the final quarter.

|

|

|

Vacancies hit 953,000 ...

Here we have updated our earlier analysis of vacancies and furlough numbers. Almost 1.0 million vacancies in the economy at the end of July, compares with 1.6 million unemployed and 1.9 million on furlough.

It will make for an interesting unwind towards the end of the year as the furlough scheme ends. In almost all sectors, the number furloughed exceeds the current level of vacancies. Health and Social care the obvious exception.

|

|

|

Borrowing levels fall ...

In the first four months of the financial year, borrowing fell to £69.5 billion compared to almost £140 billion last year.

The

out turn was £269 billion below the OBR forecast. The fiscal watchdog

had penciled in borrowing of £234 billion in the current financial year.

If the current trends were to be maintained, the outcome could be a

drop in borrowing levels to £175 billion.

It could even be lower ... easing the pressure on the Chancellor.

|

|

|

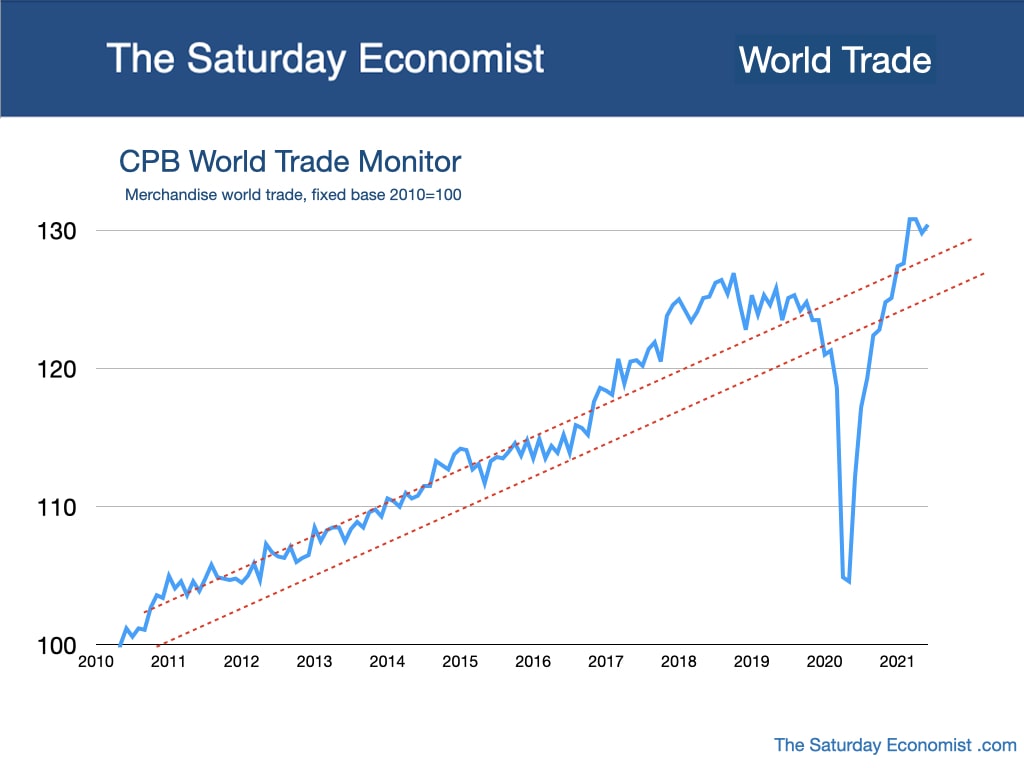

World Trade up 22% in Q2 ...

World trade bounced back, up by 22% in the second quarter of the year, following growth of 7% in the first quarter. No wonder shipping rates are soaring. Current trade levels are 5% higher than the pre-pandemic 2019 levels.

We expect growth of around 10% for the year as a whole. Shipping rates are expected to ease into the first quarter of 2022 as the rate of growth in trade slows and capacity is brought back on stream.

|

|

|

Bond Market Sentinel ... UK Ten Year Yields 0.57%.

This

is The

Saturday Economist Bond Market Sentinel, we track the performance of

ten year gilts and bonds in the US and the UK.

UK 10 year gilts yields

closed at 0.59 up from 0.52 last week. US yields closed at 1.32 from 1.26. So

much for fears of inflation and Fed tapering.

The Fed may talk of tapering but someone has to buy the debt.

|

|

|

Exchange Rate Updates ... Sterling closed at $1.38

This

is The Saturday Economist Exchange Rate Tracker. We monitor five pairs

with scenario outlook to 2022 Q1. Markets were steady in the week with

Sterling higher against the Dollar and the Euro.

The Dollar moved lower against the Euro. J Powell's statement on Fed policy did little in the markets ... |

|

|

Oil Prices Moving Lower ...

Oil

prices Brent Crude closed up at $72.58 last week. We expect oil to trade between $65 - $70 in the

second half as the long bets unwind. Is this still a realistic call? Not really!

|

|

|

Red Dots in The Sand ... When Markets Collapse

We will be back with our full markets analysis next week. I hope you had a chance to read our special update on Red Dots In The Sand.

When markets collapse.

This week David Giroux manager of the T Price $50 billion dollar US fund, decided US markets are a little too rich at current levels. The Warren Buffet Valuation index moved to a record high reflecting a near 90% over valuation compared to historical average. Interesting!

|

|

|

That's all for this special edition, let me know hat you think, have a great week ahead ...

|

|

|

|

|

|

|

© 2021 John Ashcroft, Economics, Strategy and Financial Markets, experience worth sharing.

______________________________________________________________________________________________________________

The material is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact. In particular, no reliance should be placed on the comments on trends in financial markets. The receipt of this email should not be construed as the giving of advice relating to finance or investment.

______________________________________________________________________________________________________________

If you do not wish to receive any further Saturday Economist updates, you can unsubscribe or update your details, using the buttons below or drop me an email at jkaonline@me.com. If you enjoy the content, why not forward to a friend, they can sign up here ...

_______________________________________________________________________________________

We have updated our privacy policy to address Europe's General Data Protection Regulation (GDPR). The policy changes include explaining in more detail how we use your information, including your choices, rights, and controls. We have published a GDPR compliance page about the regulation and the steps we have taken as part of our compliance process. Your privacy is important to us.

For details of our Privacy Policy and our Terms and Conditions check out our main web site. John Ashcroft and Company.com

_______________________________________________________________________________________________________________

Copyright © 2021 The Saturday Economist, All rights reserved. You are receiving this email as a member of the Saturday Economist Mailing List or the Dimensions of Strategy List. You may have joined the list from Linkedin, Facebook, Google+ or one of the related web sites. You may have attended one of our economics presentations. Our mailing address is: The Saturday Economist, Centurion House, 129 Deansgate, Manchester, M3 3WR United Kingdom.

|

|

|