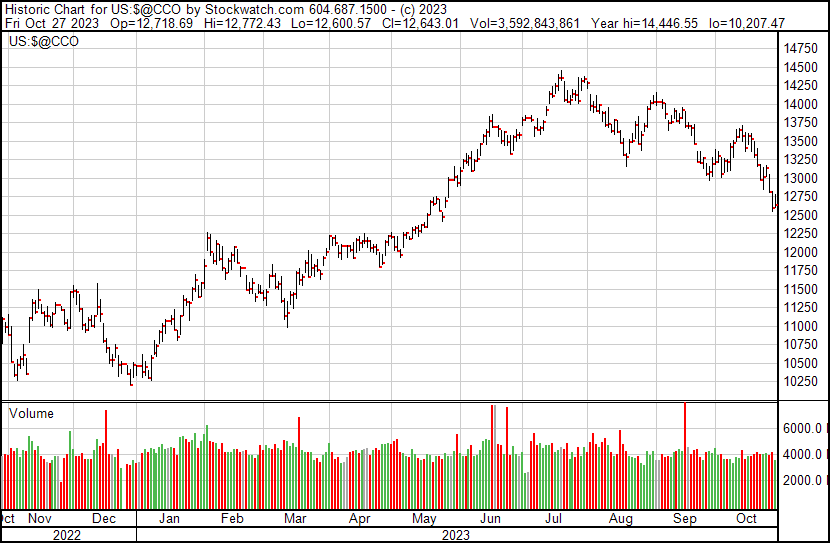

Markets It was another volatile week for North American equity markets. Poor corporate results from some of the popular names along with some hotter than expected US economic data, suggesting US interest rates may stay higher for longer, pushed markets to new multi-month lows.

The DOW was lower by 2.1%, while Nasdaq fell 2.6% and the TSX finished the week lower by 2.0%. Nasdaq has fallen by 12.5% from its year high and the TSX fell to a new 52 week low. Equity markets are well into “correction” territory. |

|

Financials Next week could be a busy week as a number of central banks, including the US Fed Bank of England and the Bank of Japan, are expected to make interest rate decisions. Meanwhile US treasury rates have been steady if not slightly to the downside. The US 10-year treasury yields have dropped by 25 basis points over the past 2 weeks. Equity markets have been feeling the strain of higher treasury yields and seem to have finally succumbed to that pressure. Lower yields would be a welcomed sight for many equity investors. |

|

In Canada, softer economic data has allowed the much watched Canada 5-year bond yield soften to the lowest level in the past 30 days and is now lower by 40 basis points from its recent high. A welcomed sight to those looking to get a new mortgage or renew their existing mortgages. |

|

And a weaker economy and weaker yields compared to US equivalents keeps effecting the Canadian dollar. The Canadian dollar touched new 52 week lows versus the US dollar this past week. Great news for Canadian exporters but bad news for those buying higher priced US goods. |

|

Commodities Oil prices eased throughout the week. Higher US oil inventories, some weaker global economic data was enough to offset the geopolitical tensions in the Middle East and WTI oil settled the week at $85.00 per barrel. |

|

|

Natural gas prices continue to be volatile and pressure on prices appears to be to the upside of late with prices trading back above $3. We are back to seeing 10%+ swings in weekly prices for North American gas prices. |

|

Drilling activity was little changed according to Baker Hughes. This past week we saw 1 rig added to the active list in the US and a drop of 2 rigs in Canada.

Gold in firmly back in the spotlight having broken back above the psychologically important $2000 mark. Heightened geopolitical tensions are outweighing higher treasury yields and strong US dollar. |

|

Stocks Up until recently I was struggling to understand why we were seeing such strong equity markets while treasury yields were rising rapidly. Big stock valuations did not make any sense to me. Most of the recent market move higher was on the back of strong stock performance of the “Magnificent 7”, Google, NVIDIA, Facebook, Amazon, Microsoft, Apple and Tesla. This past week several of these companies reported and they did not live up to their valuations. We saw significant price drops in shares of Google and Tesla as both companies’ financial results or forecasts disappointed. |

|

Google dropped roughly $180 billion in value this week. Even with the recent drops in some of these big names I still struggle to justify current valuations. I still view the valuations of many profitable and growing nanocaps we are finding to be much more compelling. Big stocks continue to look overvalued to me while many smaller companies seem undervalued.

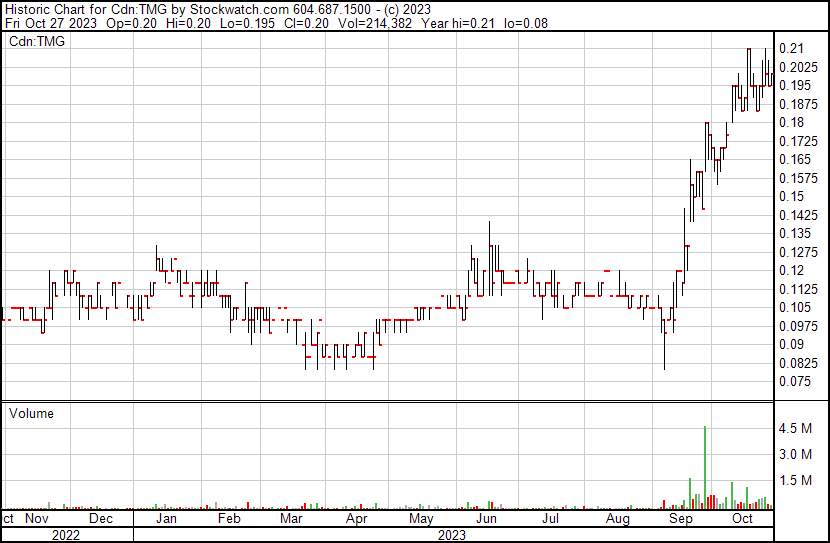

We had one of our new favorites, Thermal Energy, (TMG.V) report Q1 results this past week. The seasonally weakest quarter saw revenue growth of 66% to $5.2 million with gross profit more than doubling to $2.8 million. Earnings saw a $671,000 improvement from Q1 2023 resulting in profit of $152,000. The company also reported an order backlog of $11.6 million as of August 31, 2023, and $22 million as of October 24, 2023. This is now the company’s third consecutive quarter of profitable operations. |

|

I continue to believe that current prices do not properly reflect the growing value of the business and while I expect the stock to consolidate its recent jump in share price we view current prices as extremely attractive for longer term investors.

Statistics have shown that one of the most accurate bullish signals for a stock is when a CFO buys shares in the company they work for. There are a number of reasons why this type of action should be viewed as bullish. Of course anytime an insider is buying shares that’s usually a good sign as you would expect that means they think the stock is cheap or they expect some good news in the future. But unlike most other insiders the CFO is a bit more of a potential “tell”. CFO’s have a better understanding of a company’s financial health and future financial health and even possible funding requirements. They should have a good idea of what kind of financial commitments are needed and the companies’ ability to meet them. And let’s be honest, most accountants we know tend to be cheap… So when they spend their own money to buy shares we should raise an extra eyebrow and notice.

This past week one of our biggest dogs of the year, Immunoprecise Antibodies (IPA) not only had their new CFO buy, but so did the CEO and one of their new directors. Seeing the new director buy shares was a very welcome sign. Seeing the CEO buy more shares was also nice to see. But when I saw the CFO buy shares I turned significantly more interested. The life science sector has been crushed over the past 2 years, very few companies have escaped investor’s wrath and while IPA has been no exception the company clearly needs to improve on its business execution. A new board is likely to be voted in at their upcoming AGM. With new oversight on management I expect to see that better execution but the signs from these new buyers may be telling us that they expect it too.

Investor sentiment can be a funny thing. Two weeks ago, many IPA investors were catatonic. The sentiment was so poor that you saw all time lows in share price, a price that made little fundamental sense to me. A bit of good news, a bit of important insider buying and sentiment changed enough to see a 70% swing in share price from the week’s low to the week’s high. |

|

While this swing in price is a welcome sight, we are still a far way off from the stocks 52 week high. At Friday’s close of $1.82 the stock is off 69% from its 52 week high so while we still have a big hill to climb it’s nice to see the stock take a few steps in the right direction. The stock still appears to be fundamentally underpriced to me but the company does have to show it can execute and deliver on its promise.

This past week we also saw news from Total Telcom (TTZ.V) * announcing another RV control order. This was its third order and continues to showcase the company’s ability to sell some of its newest products. Neil Magrath, chief executive officer of Total Telcom, commented: "Our expanding interest and adoption from the marketplace for our RV controllers has resulted in another follow-on order from our distributor. We continue to receive positive feedback from our distributor for our controllers, and the successful rollout of the second-generation products continues to make steady progress."

I added to my Total Telcom holding, buying shares at $0.43 and $0.445 on Friday on the dip. |

|

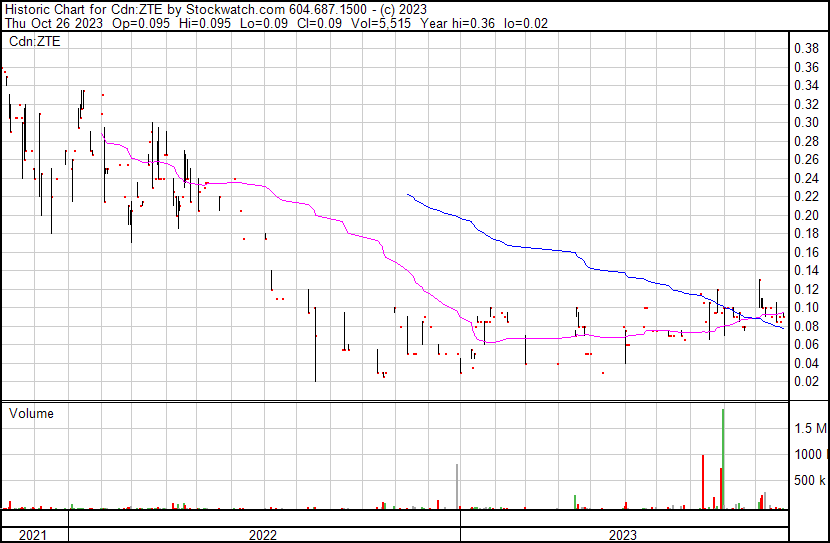

The other company from our nanocap universe and recent “Cheapies” list reporting on Friday was Ztest Electronics (ZTE.V). Revenues were higher by 7.2%, net income was higher by 50%. This is the second consecutive quarter of profitability for Ztest. |

|

We saw three of our Cheapies with a Chance hit new 52 week highs this past week. AirIQ (IQ.V)… |

|

California Nanotech (CNO.V)… |

|

And Spectra Products (SSA.V). |

|

And while not a new 52 week high one of other Cheapies, Nova Cannabis (NOVC.T) put in a precent decent week and moving up 35% since inclusion in our CWAC list. |

|

Other Stuff So last week I wrote a bit about one of our key search criteria we use to find new investing ideas, growth. This week I want to talk a bit about another key criteria we look for when it comes to identifying strong investment candidates, profit. |

|

Most microcaps and early stage companies do not generate profits. Many have gone public to help raise equity capital until they can become self sustaining. We look for that smaller percentage of companies that have broken out and started to make profits, real cash profits. Why do we find a company’s profitability as so important? I often say there are two types of companies, those that generate cash and those that don’t. A company that generates its own cash has a significantly different risk profile that those that lose money. It tends to be significantly less risky than a company that continues to lose money. Profit confirms that a company can sell enough of its products or services in a way and at a price that generates a profit. Profits can also allow for cheaper cost of capital. Lenders are much more willing to lend and with more favorable terms when a company can show it can repay loans thru the profit stream of the company.

And profit growth is usually levered to the revenue growth of the company. In most cases profits grow faster than revenues. So, a company that is growing revenues quickly usually sees an even faster rate of profit growth.

A company generating profits has greater control of its future as it is much less likely to need to finance future growth. This means there is much less financing or dilution risk. Dilution is the silent destroyer of microcap upside. A company that continues to raise equity capital dilutes away your ownership and dilutes away your upside. Profitable companies can increase growth when they deploy excess cash from profits to grow the business thru more research and development spending, more hires, acquisitions, more purchasing more equipment. And excess cash can also be used to buy back shares which actually increases your percentage ownership and increase your upside. Profits can allow the business to compound value if effectively re-invested.

Not all profit is equal. We want to see high quality profit meaning profit that is converting to cash. Sometimes companies have a hard time collecting on receivables and profit doesn’t run to cash or it could take a long time to collect the cash. This makes these profits less valuable than a company that collects quicker and can re-use that profit. We also prefer to see high margins. High gross profits margins and high profit margins. High margins can give the company more flexibility and a better risk profile.

We want to see profits, but we also want to see growing profits. As we said last week, growth is extremely important if we want a high chance of finding outperforming companies. Growth in revenues and growth in profits. So, not only do we want a profitable company we look for companies growing profits by at least 25%. Of course, the faster the rate of profit growth the better. And we want to see that 25% growth to be in earnings per share. A company issuing shares at that the same rate of growth as the companies profits rarely improve the value for shareholders.

Ok, so there you have it. Profits are an extremely key criteria when we are searching for new investment ideas. We have thousands of stocks to choose from and we have seen many statistics and even our own experience that tells us that profitable and growing microcaps, that are priced appropriately, can give you the best opportunity for multi-bagger style returns. By just sticking to profitable companies I believe you greatly improve your risk/reward outlook for your portfolio and dramatically increase your chance to find long term winners.

Strong revenue growth combined with strong profit growth at a reasonable or better valuation is key to finding multi-baggers consistently. But what do I mean by reasonable or better valuations and how do we determine that? That’s what I’ll talk about next week.

To your wealth, Paul and Trevor |

This Week’s Buys and Sells

Bought Total Telcom (TTZ.V)* at $0.43 and $0.445 *Paul Andreola is a director of Total Telcom (TTZ.V) |