And speaking of buy outs… I spoke with a colleague of mine in New York, and we got to talking about the markets and what I am seeing up here in Canada. He was quite surprised by some of the microcap valuations that I mentioned. His immediate reaction was “Why is no one buying these companies and taking them private?” It was a bit of a tough one to answer. I believe we will see more go private transactions. The recent announcement that the Canadian government will start taxing company share buy backs was probably another incentive to take these small, profitable companies private.

If I’m the manager and significant shareholder of a small public company in Canada, I have to ask myself why stay public if investors won’t fairly value my business? With less tools at my disposal to correct my market value what benefit do I get in being public. The whole idea of being a public company really stems around the fact that public companies are traditionally valued higher than private market comparables, and this allows for lower cost of equity capital if a company needs it. But what if a company doesn’t need capital as is the case with so many of these great little companies? And if the company is a roll up business like Atlas Engineered Products and investors value you less than companies are being sold for in the private market, what’s the point in having a publicly trading currency?

Now add in the ongoing costs of being public, exchange filing fees, regulatory and financial filing fees, legal and consulting fees, investor relations costs and now a dramatically higher cost for annual audits Audit fees have exploded this year and it’s not unheard for these fees to have tripled and that is IF you can find an auditor to take on these “small” clients. I know of one small company whose audit fees went from roughly $40,000 to over $120,000 this past year. Add the time and manpower needed to oversee and manage these items. The cost can easily start to add up to +$500,000 for a decent little nanocap. This is cash that basically would fall straight to the bottom line.

It’s no wonder many CEO’s we speak to are so frustrated with their company share price. I’m hearing more discussions about going private and fears of hostile takeovers. Over the past few weeks Thunderbird Entertainment has become the target of dissident shareholders who want to takeover the company’s board to look at selling the company to a larger entity. Without the usual public market premium, I think we will see many companies being swallowed up by larger players, hostile takeovers or taken private by management, this in turn should spur better valuations for these companies and likely reinvigorate investor interest in similar companies. These cheap companies getting taken out at healthy premiums is usually one of the triggers to start a new bull phase in the market or sector.

Many of the companies I own fit into this category. They are healthy growing businesses that are starting to make much more sense as private businesses. Adding $500,000 to the bottom line can be big incentive to take on the cost and effort of going private. Their value is so much more significant without the public market expenses.

As I’ve said before, the cure for low prices, is low prices.

Other Stuff

The economy continues to show signs of slowing down. Some sectors are slowing down faster than others and still some don’t appear to be slowing down at all. It’s interesting to keep seeing prognosticators talk about the stock market and economy as if it is one big animal. The stock market is a market of stocks.

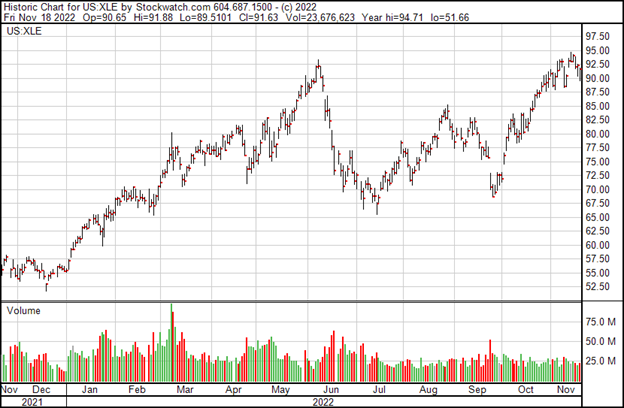

Oil stocks have had a great run this year while the market has gone down quite a bit and year to date is the only major sector to be in the positive. Traditional recession resistant sectors such as Utilities, Healthcare and Consumer Staple sectors are down but have done considerably better than the overall market. Communication services, Technology and Real Estate round out the market’s bottom performers. Within these sectors there are sub sectors and stocks that have done considerably better and worse than their group.

My point in this is that to be successful as an investor, especially a microcap investor, you need to find a way to avoid the noise and headlines and drive down to the data that allows you to be one step ahead of others. You need to be proactive with your investments and less reactive to noise…. specially to headline news. I continue to be amazed at how many people are still talking about stocks and strategies that worked in the last bull market.

“Generals are always prepared to fight the last war.” Winston Churchill.

The next bull market will be different than the last bull market. Strategies need to be prepared for what lies ahead. We need to be aware of new trends. Do you have a strategy to find and monitor these new trends?

Look for signs of strength. Sector strength and clusters of certain kinds of stocks showing strength. I keep an eye on new Nasdaq and TSX 52-week highs.

Strength is not always about stocks going up as much as weakness is not always about stocks going down. Sometimes what is important to note is relative strength or relative weakness.

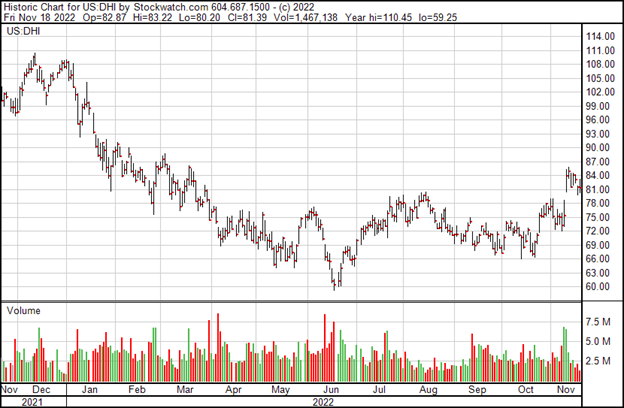

One sector that I continue to watch very closely, for obvious reasons, is the housing sector. Interest rates have spiked at one the fastest rates in history. As can be expected US housing data has turned significantly bearish. The headlines have been as bearish, if not more bearish, than what I remember during the great financial crisis of 2008/2009. Yet, the sector stocks have held up considerably well under these circumstances. Could it be that many investors are fighting the last war?