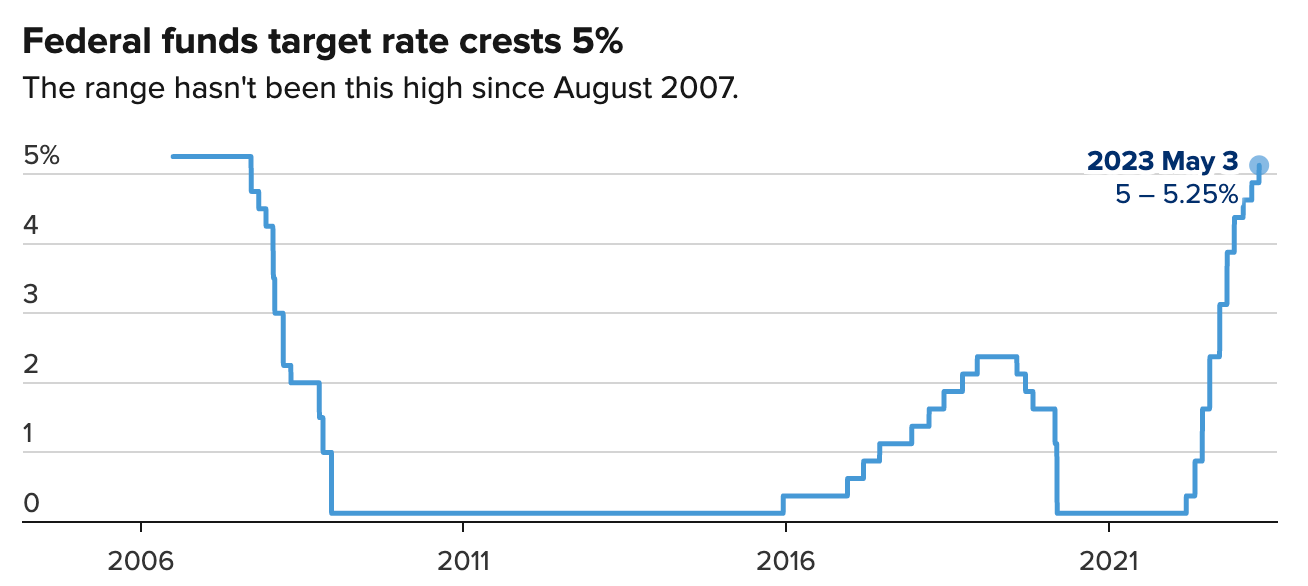

Markets This past week we had the much anticipated US Federal Reserve decision on interest rates and as expected they delivered a 25 basis point increase and stated that a pause at the next meeting is likely. Fed fund rates are now at their highest levels since 2007. |

|

However, markets continue to price in potential rate cuts in the next few months. Equity markets were initially lower on the news but rallied by week’s end with Nasdaq gaining 2.2% on the day. For the week Nasdaq was higher by 0.1% while the DOW was down 1.2% and the TSX lower by 0.5%. |

|

Investors will be watching for further economic data to decide whether they should expect the Fed to change its current wait and see stance.

Financials The US dollar, measured by the DXY, saw little in the way of change this week. It continues to trade near lows of the year and is painting a picture of an economy that is not too hot and not too cold. You’d think that with the current US regional banking crisis and US government debt ceiling arguments we’d see more volatility in the dollar. |

|

Treasury yields were lower on the week as investors weigh the recent Fed moves and the additional regional bank struggles. It’s become pretty clear that the tighter Fed rate environment and recent runs on several banks have investors sensing that the Fed doesn’t have much room to move higher at this stage. |

|

In Canada the 5 year bond yield was lower on the week, however it spiked on Friday and closed just a tad above 3%. |

|

Commodities Gold had a solid week closing back above US$2000 per ounce. A tepid US dollar and further belief that the US Fed is close to halting interest rate hikes has gold bulls back in charge of the yellow metal. |

|

WTI oil was lower on the week and closed at $71.34. Oil did trade below $70 for a few days and continues to frustrate oil bulls as the price is now significantly lower than when OPEC+ announced their production cuts and far below the levels we saw at the commencement of the Russian invasion of Ukraine. |

|

With lower energy prices it’s understandable to see continued slowdown in North American drill rig activity. According to Baker Hughes drill data we saw another drop of 7 rigs this past week, all 7 from the US side of the border.

Stocks We continue to see nice pockets of strength in certain sectors of our microcap universe. If you own the right kind of microcap stocks, fundamentally sound, growing and profitable, you’re likely seeing more green than red lately. The bulk of the winning names I’m seeing continue to be in the “boring is beautiful” manufacturing sectors. Firan Technology (FTG.T), Data Communications Management (DCM.T), H2O Innovations (HEO.T), and Atlas Engineered Products (AEP.V) all hit new 52 week highs this past week. |

|

These types of share price moves have been encouraging institutions to look down market and we are seeing increased liquidity in many of these names. Usually, many larger players like to get their positions by buying into financings when the companies are out looking for money to grow. Data Communications Management this week announced they’ll be raising $25 million in equity financing, no doubt on the back of strong institutional interest in the company’s shares. What gets interesting is that most of these companies don’t need to raise equity and if institutions want in they are going to have to buy in the open market forcing prices higher and adding buyside liquidity. |

|

Financings like this are a sign that institutional money, which for the most part has stayed in larger liquid names, is starting to venture down market where we like to play. We welcome them on over!

Ok, this is the part of my article where I talk about the housing sectors…..again. This past week we saw financial results from Builders FirstSource (BLDR). Revenues were down almost 32% and earnings were down 48% from the year ago period. You’d think that these numbers would have hurt the stock but the stock these numbers actually blew away expectations. The stock closed the week up 17% reaching another new 52 week high. |

|

According to Rick Palacios Jr, Director of Research at John Burns Research and Consulting, in the US nationally, builders now expect new home sales to rise by 7% in 2023. When they were asked this same question back in November 2022, builders thought sales would drop by 9% in 2023. Expectations have taken a big shift upwards.

This sentiment along with the stronger than expected results from a number of US home builders and construction related companies has driven the home builder ETF (ITB) to new 52 week highs. |

|

Remember, markets are forward looking, and the better than expected results combined with building pent up demand and markets starting to bet on central bank potential loosening of interest rates has some investors forecasting a very strong outlook for these companies and with similar dynamics at play in Canada on top of an even more rapidly increasing population north of the border, the few construction related listed companies here could surprise investors even more.

That’s all I’ve got for this week. To your wealth, Paul and Trevor |